Best 529 Plans for Newborns vs Trump Accounts: What New Parents Open in 2026

Picture this: It’s 3 a.m., your newborn finally drifts off—and soaring tuition costs jolt you awake. Four-year sticker prices already race past six figures and keep climbing. The upside? Parents now wield two high-octane savings engines.

First is the proven 529 plan, a state vehicle where money grows tax-deferred and qualified withdrawals stay tax-free. Second is the coming federal “Trump account,” set to launch mid-2026 with a $1,000 head-start for every eligible baby. Combine them and you marry tax perks, free seed money, and decades of compounding.

For a quick refresher, see Comparing ways to save for college, then let’s map out your smartest first moves while the crib mobile still spins.

How 529 plans and “Trump accounts” work

1. 529 college savings plans: your tax-free tuition engine

A 529 plan is a state-sponsored account that lets your after-tax contributions grow tax deferred and come out tax-free for qualified education. Most states add a deduction or credit on what you put in, scoring a guaranteed return before the market even moves.

You stay in control of the money. You decide when to withdraw, and you can switch the beneficiary to a sibling, cousin, or even yourself if goals change. Beginning in 2024, families may roll up to $35,000 of leftover 529 funds into a child’s Roth IRA after 15 years, keeping the tax shelter alive instead of paying penalties (Washington Post, 2025).

Federal rules let you open any state’s plan and spend the funds at almost any accredited college or trade school. Capture your home-state tax break first; if your state offers none or charges high fees, choose one of the national low-cost standouts we rank next (CNBC Select, 2025).

Account minimums have vanished. Start with the cost of a pack of diapers, turn on automatic drafts, share the gifting link with grandparents, and let compound growth work while you focus on sleep training.

2. “Trump account”: a $1,000 head start that grows with your child

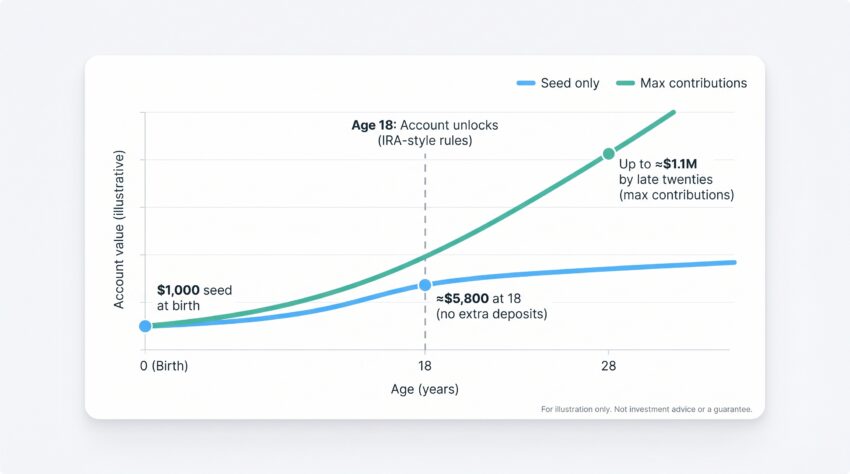

Every baby born from January 1, 2025, through December 31, 2028, qualifies for a federally funded investment account seeded with $1,000 and invested in a low-cost index portfolio. Fox Business reports that enrollment, opening nationwide in July 2026, takes only minutes.

The funds are locked until age 18, shielding them from impulse taps and giving the seed time to grow. White House Council of Economic Advisers projections show the initial $1,000 could reach about $5,800 by high-school graduation, and families that max out contributions may see nearly $1.1 million by a child’s late twenties.

At eighteen, ownership shifts to the student and the account adopts IRA-style rules. Money can cover tuition, a first home, or stay invested for retirement. Qualified uses avoid the early-withdrawal penalty, though earnings are still taxed as ordinary income.

The playbook is simple: claim the free $1,000 first, then decide how much extra to add once program details are final. Think of the Trump account as an all-purpose launchpad and the 529 as your pure tuition engine.

Next, we’ll rank the five state 529 plans that combine rock-bottom fees with generous incentives.

The seven smartest college-savings moves for newborns

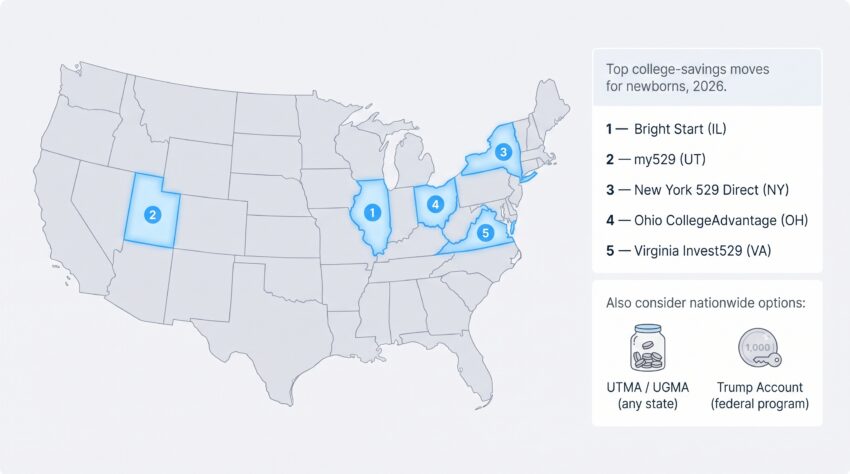

1. Bright Start 529 College Savings (Illinois): best overall value

Bright Start tops the list because it gives you more growth per dollar than any other plan we reviewed.

Cost first. Illinois cut portfolio expenses by about 13 percent in late 2024, dropping many age-based options near 0.10 percent a year (CNBC Select, 2025). Over 18 years, even a half-point fee gap can erase thousands in compounding.

Now the tax carrot. Illinois residents can deduct up to $10,000 ($20,000 for couples) each year. At a 5 percent rate, that is an automatic $500 on a full contribution.

New parents get an extra $50 through the First Steps program, signaling a state committed to early momentum.

Practical wins seal the deal. No minimum to open, a quick online application, a mobile app for balance checks, and gifting links for grandparents.

Live elsewhere? If your state offers no deduction or higher fees, Bright Start still shines.

Side-by-side charts at Comparing ways to save for college show exactly why a 529’s tax-free withdrawals, high contribution caps, and lack of income limits usually beat Roth IRAs and plain savings accounts. Review them first and the case for Bright Start’s low-fee 529 nearly makes itself.

2. my529 College Savings Plan (Utah): ultra-low fees with DIY flexibility

Think of Bright Start as the family sedan; Utah’s my529 is the sports coupe—efficient and fully under your control.

Default age-based portfolios cost about 0.13 percent a year, letting more of each contribution work from day one.

Tinkerers can build custom mixes from Vanguard and Dimensional funds. Four preset glide paths handle things automatically if you prefer hands-off. No minimum to open.

Utah residents earn a 4.45 percent credit on contributions. Non-residents still benefit from one of the nation’s cheapest plans, plus a slick gifting portal and responsive support.

3. New York’s 529 Direct Plan: Vanguard simplicity you can trust

Parents who want both rock-bottom fees and a household name find it here. Every portfolio uses Vanguard index funds, keeping the total expense around 0.13 percent.

Open online in minutes, skip the minimum deposit, and choose an age-based track that glides toward bonds as college nears.

New Yorkers can deduct up to $5,000 ($10,000 for couples) from state income yearly. Residents of states with no 529 break still flock here for cost and brand strength.

4. Ohio CollegeAdvantage: wide fund menu plus a family-friendly tax break

CollegeAdvantage balances choice and clarity. Two age-based tracks built from Vanguard index funds keep most fees below 0.20 percent. A separate lineup adds Dimensional options, a stable-value fund, and even a cash portfolio.

Ohio residents can deduct up to $4,000 per beneficiary each year, with excess contributions rolling forward indefinitely. Over 18 years, that can shelter more than $70,000 from state tax.

Start with $25, automate as little as $25 a month, and track progress in a clean dashboard that updates with every market move.

5. Virginia Invest529: feather-light fees for set-it-and-relax savers

Virginia’s direct plan proves low cost and strong governance can coexist. Many enrollment-year portfolios charge under 0.15 percent—far below the 0.40 percent national median.

The state agency negotiates institutional pricing and passes savings to families, earning consistent top ratings from Morningstar.

Pick the enrollment year that matches freshman fall, and the mix shifts automatically. Sector slices and real-estate tracks are available for variety, still at bargain prices.

Virginia residents can deduct up to $4,000 per account each year, but the plan also attracts out-of-staters who want the ultralow expenses. Open with ten dollars, switch on automatic drafts, and let compounding work while you hunt for sleep.

6. Custodial brokerage account (UTMA/UGMA): ultimate flexibility, higher aid hit

A 529 locks money into education; a UTMA keeps every door open. You can hold stocks, bonds, ETFs, or even crypto, and withdrawals may cover any expense that benefits your child.

The trade-off is tax treatment. Earnings above $2,700 each year are taxed at your bracket, and FAFSA treats custodial assets as the student’s, assessing up to 20 percent annually (CNBC Select, 2024). Control shifts at 18 or 21, depending on state.

When a UTMA shines:

- You want one pot for college, trade school, or a future business.

- Grandparents prefer gifting individual stocks.

- You already max 529 and retirement contributions and still want to save.

Most families use a UTMA as a sidecar, not the main college engine.

7. Trump account: free $1,000 now, long-range wealth later

Babies born from January 1, 2025, through December 31, 2028, qualify for a federally funded Trump account seeded with $1,000 once parents enroll. Registration opens July 2026.

The money sits in a low-cost index mix and compounds tax-deferred until age 18. Even without extra deposits, projections show the seed growing to about $5,800. Maxing contributions could push balances near $1.1 million by the late twenties.

At 18, the account shifts to the student and follows IRA-style rules. Funds can pay for college or a first home, or they can stay invested for retirement. Qualified uses avoid the early-withdrawal penalty, though earnings are taxed as income.

You cannot tap the cash before 18, but that lock helps FAFSA because retirement-style assets stay outside aid formulas.

Claim the $1,000 as soon as portals open, automate what you can, and let the Trump account complement your tax-free 529.

Your top questions, answered

How much should we save each month?

Begin with an amount that feels comfortable and automate it. Saving $100 a month from birth in a low-fee 529 earning a 6.9 percent net return can grow to about $40,000 by age 18, enough to offset a solid slice of in-state tuition. Even $25 a month matters because time, not the dollar figure, does most of the work. Increase contributions with each raise, and remember you can roll up to $35,000 of leftover 529 money into your child’s Roth IRA if you exceed the goal.

What if our child skips college?

A 529 is no longer restrictive. You can:

- Change the beneficiary to another relative.

- Roll over unused funds—up to $35,000—into the student’s Roth IRA after 15 years.

- Withdraw for non-education uses and pay ordinary income tax plus a 10 percent penalty on the earnings only.

Money in a custodial or Trump account is already flexible. A UTMA can fund any goal at any age, while a Trump account unlocks at 18 and follows IRA rules, so qualified education or first-home costs avoid the early-withdrawal penalty, although earnings are taxed.

Should we stick with our state’s 529 or shop around?

Start with your state tax break. If you receive a deduction or credit, claim it on the amount you plan to contribute this year. After hitting that limit, or if your state offers no perk (looking at you, California), choose a national low-fee plan you prefer. Federal law lets you use any state’s 529 at any eligible college, so your money is never stuck across state lines.

Can we combine multiple accounts?

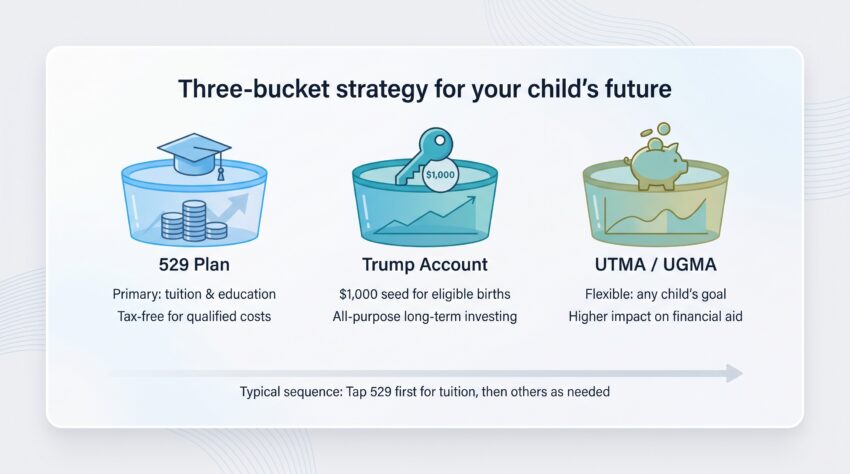

Yes. Many families use a three-bucket approach:

- A 529 for predictable tuition costs.

- A Trump account to capture the $1,000 seed and grow long-term wealth.

- A smaller UTMA for discretionary or entrepreneurial goals.

Because these accounts live under different tax codes, they do not interfere with one another or with your own retirement contributions. Coordination merely means choosing which pot to tap first when tuition bills arrive—usually the 529, since it provides tax-free withdrawals.

Will any of this hurt financial-aid chances?

Parent-owned 529 balances count as parental assets and can reduce need-based aid by up to 5.64 percent of the account value, far less than student-owned assets. Custodial UTMAs are student assets and face a 20 percent assessment each year under the federal formula. Trump accounts, structured like IRAs, stay outside the FAFSA asset tally while the funds remain inside, giving them an aid advantage.

Conclusion

The smartest play for new parents in 2026 is to stack accounts, not pick one. Open a low-fee 529 like Bright Start the week you bring baby home, claim the free $1,000 Trump account once portals open in July, and add a UTMA only if you need extra flexibility. Automate small contributions and let compounding handle the rest—your newborn graduates with options, not debt.